filmov

tv

autoregressive conditional heteroskedasticty

0:10:29

Time Series Talk : ARCH Model

0:05:14

Autoregressive Conditional Heteroskedasticity (ARCH) Model | Time Series forecasting

0:05:10

What are ARCH & GARCH Models

0:04:06

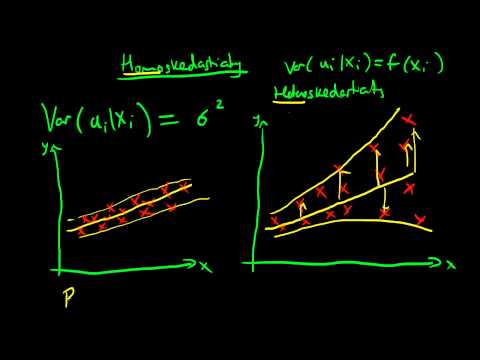

Heteroskedasticity summary

0:40:31

GARCH: Generalized Autoregressive Conditional Heteroscedasticity | Time Series Lecture 17

0:08:20

Autoregressive conditional heteroskedasticity

0:09:02

R29 Intro to GARCH, Generalized Autoregressive Conditional Heteroskedasticity, , R and RStudio

0:10:25

GARCH Model : Time Series Talk

0:21:03

The Autoregressive Conditional Heteroscedastic model

0:11:12

ARCH and GARCH Models

0:04:30

Autoregressive conditional heteroskedasticity | Wikipedia audio article

0:20:25

Autoregressive conditional kurtosis (GARCHK): Time-varying heavy tails (Excel)

0:09:57

An Introduction to GARCH Models

0:15:08

Autoregressive conditional heteroskedasticity - Wikipedia Article Audio

0:07:12

Lesson 31c Conditional Autoregressive Models

0:10:39

Autoregressive Conditional Heteroscedasticity with Estimates of the Variances of UK Inflation Rates

0:07:00

CFA® Level II Quantitative Methods - Heteroskedasticity: Why it is a problem and how to detect it

0:08:29

Generalization of ARCH: Theoretical introduction to GARCH

0:50:17

Econometrics for Finance - S6 - Volatility Models

0:12:13

HAR model explained: Heterogeneous autoregressive volatility (Excel)

0:11:12

GARCH Model in R with simple explanation

0:06:32

GARCH Volatility Model

0:17:49

ARCH model - volatility persistence in time series (Excel)

Вперёд

0:10:29

0:10:29

0:05:14

0:05:14

0:05:10

0:05:10

0:04:06

0:04:06

0:40:31

0:40:31

0:08:20

0:08:20

0:09:02

0:09:02

0:10:25

0:10:25

0:21:03

0:21:03

0:11:12

0:11:12

0:04:30

0:04:30

0:20:25

0:20:25

0:09:57

0:09:57

0:15:08

0:15:08

0:07:12

0:07:12

0:10:39

0:10:39

0:07:00

0:07:00

0:08:29

0:08:29

0:50:17

0:50:17

0:12:13

0:12:13

0:11:12

0:11:12

0:06:32

0:06:32

0:17:49

0:17:49